Understanding Inventory Valuation

February 23, 2026

February 23, 2026

Inventory valuation is a critical step for any business that manages goods or raw materials.

How do you accurately determine the true value of your inventory? Which method should you choose to reflect your company’s financial position correctly? For small and mid-sized businesses, inventory valuation directly affects profitability, cash flow, and strategic decision-making.

In this article, we break down inventory valuation, its challenges, the main methods available, and best practices for integrating it effectively into your business management.

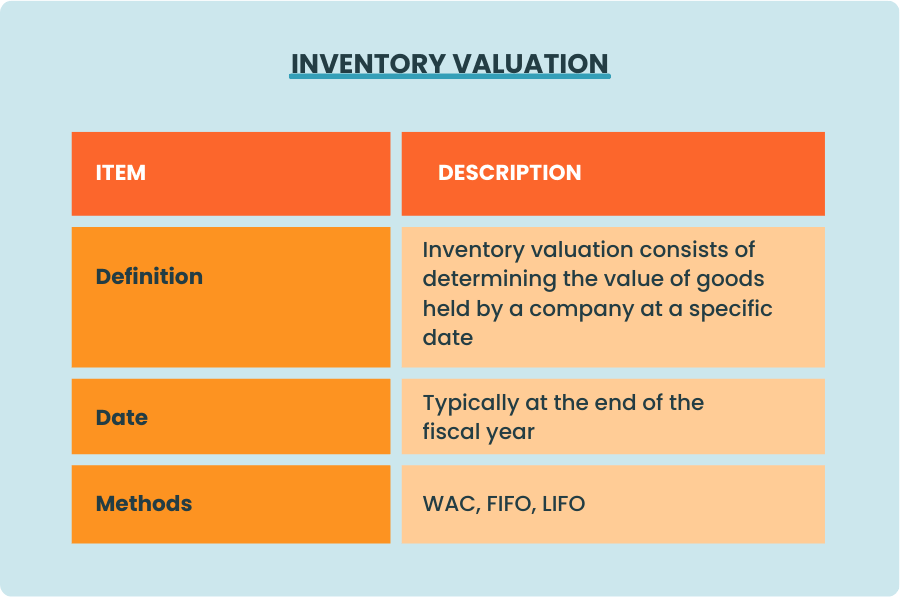

Inventory valuation refers to the process of determining the actual value of goods, finished products, or raw materials held by a company at a specific date, typically at the end of the fiscal year.

For trading companies, this means assessing the purchase cost of products still in stock. For manufacturers, the logic differs slightly: inventory is valued at production cost, which includes raw materials, direct labor, and certain overhead expenses.

The objective is straightforward: present a fair and accurate view of the company’s assets on the balance sheet. Inventory often represents a significant portion of total assets. An inaccurate valuation can distort the company’s financial position.

Beyond regulatory compliance, properly valuing inventory provides clear visibility into what capital is tied up, what truly generates margin, and what impacts cash flow.

First, inventory valuation directly impacts net income and gross margins. Accurate valuation is essential for informed decision-making.

Second, inventory frequently ties up a substantial amount of working capital, which can strain cash flow. Without precise visibility into its real value, it becomes difficult to decide between restocking, running promotions to reduce stock, or adjusting purchasing volumes.

Finally, it plays a central role in operational management. Knowing the value of your inventory allows you to analyze turnover, identify slow-moving items, and optimize purchasing. For SMBs, this translates into reduced overstocking, fewer stockouts, and improved margin control.

Under most accounting frameworks (including US GAAP), several inventory valuation methods are recognized. The most commonly used methods for SMBs are FIFO (First In, First Out) and Weighted Average Cost.

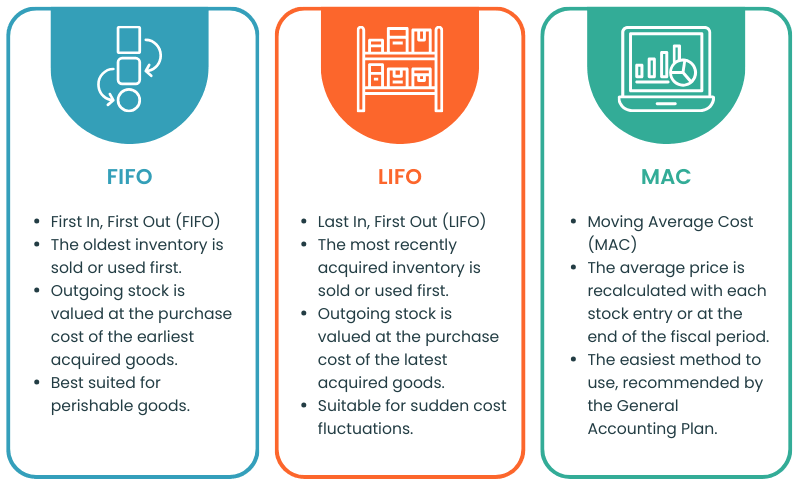

The FIFO method is based on a simple assumption: the first items purchased are the first items sold.

In practical terms, ending inventory is valued using the cost of the most recent purchases. This approach often aligns with the physical flow of goods, especially for perishable or fast-moving products.

In an inflationary environment, FIFO generally results in higher ending inventory values because the most recent purchases tend to be more expensive. As a result, the inventory valuation more closely reflects current market conditions.

FIFO is widely appreciated for its intuitive logic and consistency with actual inventory flows.

The Weighted Average Cost method calculates an average unit cost for all items in inventory.

The idea is to smooth out price fluctuations by computing a new average cost each time inventory is replenished (or at the end of a period, depending on the system used). This method is particularly relevant when purchase prices vary frequently.

In practice, WAC stabilizes inventory valuation and reduces significant variations between reporting periods. For businesses facing regular supplier price changes, this method offers a more consistent financial view.

The LIFO method (Last In, First Out) is the opposite of FIFO: it assumes that the most recently acquired or produced items are the first ones sold.

In practice, ending inventory is valued using the cost of the oldest items in stock. During inflationary periods, this generally results in higher Cost of Goods Sold (COGS) and lower reported net income, since the most recent and often more expensive purchases are recognized first.

LIFO is permitted under US GAAP and is commonly used in the United States, particularly in industries exposed to price volatility. However, it is not allowed under IFRS and is therefore prohibited in most international markets.

Because it can significantly impact profitability, taxes, and balance sheet presentation, LIFO requires careful consideration, especially for companies operating across multiple jurisdictions.

The right method depends primarily on your business model and the nature of your products.

If your purchase prices are relatively stable and your inventory flow naturally follows a chronological order, FIFO may be appropriate. It provides an ending inventory value close to recent costs.

If supplier prices fluctuate frequently and you prefer a more stable approach over time, Weighted Average Cost may be more suitable.

It is also important to consider your tracking capabilities. Some methods require precise monitoring of inventory movements. For SMBs, using a dedicated inventory management system greatly simplifies consistent application of the chosen method.

Inventory valuation is mandatory at the end of each fiscal year. It directly affects both the balance sheet and the income statement.

Consistency is essential. The same valuation method should be applied from one fiscal year to the next to ensure comparability. Any change in method must be justified and properly documented.

Accurate inventory valuation supports reliable financial reporting and strengthens discussions with accountants, investors, and lenders.

Inaccurate valuation can have several consequences.

Overvaluing inventory may create an artificially positive picture of performance. While it may appear beneficial in the short term, discrepancies can quickly surface during audits or financial reviews.

Undervaluing inventory, on the other hand, may unnecessarily reduce reported profits and distort key performance indicators.

There are also tax implications. Incorrect valuation can lead to errors in taxable income reporting.

Operationally, unreliable data complicates purchasing and production decisions. Without dependable visibility, management becomes reactive rather than strategic.

Inventory valuation should not be viewed solely as an accounting requirement.

Choosing the right method, applying it consistently, and relying on accurate data helps protect margins, optimize purchasing, and manage cash flow more effectively.

This is precisely where Stockpit adds value. Designed for SMBs, Stockpit enables real-time inventory tracking, reliable data management, and cost monitoring based on your selected valuation method. Decision-makers gain clear visibility into margins and the true value of their inventory.

Say goodbye to stockouts! Get your inventory valuation, monitor the inflow and outflow of products and keep track of your inventory.